Did Bank of Japan crash the dollar?

The consequences of 26 years of free money policy and aggressive Quantitative Easing (read: money printing) are coming due. The United States is among the most vulnerable to Japanese contagion.

Originally published at I-System TrendCompass on 28 Jan. 2026.

Over the last nine days, the US dollar index collapsed: on 19 January, the index closed at 99.16. Today it is trading below 96 - a 3.2% decline! This may not sound like much, but as far as foreign currency markets are concerned, it’s a very substantial move:

The culprit may have been the Bank of Japan. Over the last 26 years, Japan has been the world’s key exporter of financial capital. The Bank of Japan (BOJ) made money free in 1999 (setting interest rates at zero) and pioneered quantitative easing (QE) in 2001. With interest rates at or near zero and vast quantities of liquidity generated out of its printing presses, the BOJ became the world’s largest owner of Japanese Government Bonds (JGBs) as well as U.S. Treasuries.

Bank of Japan owns some 52% of all JGBs outstanding and around $1.2 trillion in U.S. treasuries (as of October 2025). In effect, the BOJ has been monetizing government debt. In the process, Japan has accumulated the highest ratio of public debt to GDP of any developed country: a whopping 260%. In other words, Japan’s public debt is now 2.6 times the size of the annual output of her entire economy.

The “carry trade” unwind tsunami

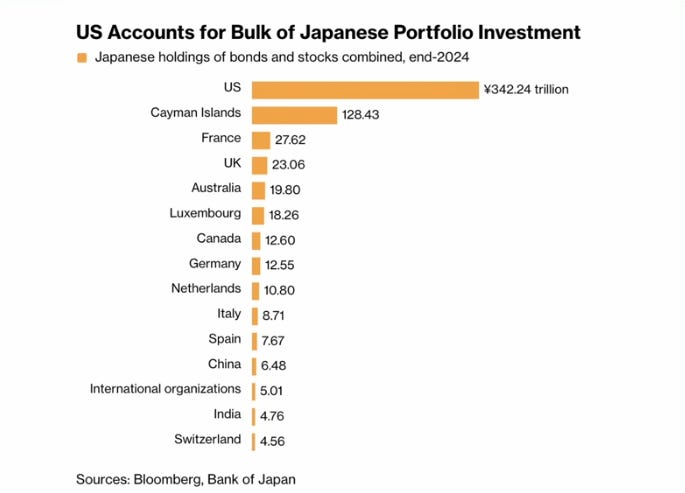

Japan has also been the source of the so-called carry trade: Japanese and foreign investors borrowed funds in Japan at very low interest rates, and invested them elsewhere around the world where return on capital was considerably higher. By today, Japan’s $7 trillion JGBs market has been the ultimate source of the colossal carry trade exposure that could cause unprecedented market turmoil. U.S. markets could be among the most vulnerable. According to Bloomberg, U.S. carry trade exposure totals some 342 trillion yen, corresponding to about 2.25 trillion U.S. dollars.

There’s no means of avoiding the final collapse

All these balances accumulated during the “good old days” of zero interest rates when market participants didn’t have a care in the world about the bulging debts: it was all free money, going around in nearly unlimited amounts. But as Ludwig von Mises correctly pointed out,

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.

Today, the reversal of Japan’s zero interest rates policy and all that it entailed, is accelerating. This month, the yield on 10-year JGB hit over 2.3%, the highest level since 1997. Now, the cost of servicing Japan’s public debts consumes around 25% of the government’s budget. Rather than providing economic stimulus, the Bank of Japan has reversed its QE policy and has begun aggressively reducing its colossal balance sheet.

One of the unintended outcomes of BOJ’s aggressive QE policy has been the steady depreciation of the yen, in spite of rising interest rates. Now, to defend the yen and to keep their bonds markets from collapsing, the BOJ and other Japanese financial institutions must scramble to repatriate their foreign investments, including stocks, bonds, ETFs and ultimately even US government treasuries, since they represent the largest and most liquid foreign asset Japan owns. In a crisis, Japan will be forced to liquidate their US Treasury investments.

Western nations will follow Japan’s policies

This is an inevitability, as Ludwig von Mises predicted. The ultimate consequences of this crisis would be difficult to forecast, but given the magnitude of imbalances that are now present in global markets thanks to 26 years of Japan’s massive QE, the contagion from Japan could hit the whole global economy like a tsunami. In response, the governments of other Western nations might have to resort to the same policies as the BOJ.

When Japan yanks liquidity from under their markets, their central banks will have to ramp up their own printing presses that much more. Ultimately, this process leads to an acceleration of inflation and/or hyperinflation. And by now, every overindebted government will welcome inflation as it will enable them to get rid of their debts with a worthless currency.

Alex Krainer – @NakedHedgie is the creator of I-System Trend Following and publisher of daily TrendCompass investor reports which cover over 200 financial and commodities markets. One-month test drive is always free of charge, no jumping through hoops to cancel. To start your trial subscription, drop us an email at TrendCompass@ISystem-TF.com, or:

NEW: Check out our daily TrendCompass on Substack, covering 18 key global markets, incl. gold and bitcoin at under $1/day

For US investors, we propose a trend-driven inflation/recession resilient portfolio covering a basket of 30+ financial and commodities markets. Further information is at this link.

Hyperinflation on cue, leading to CBDCs....

Aside from a vehicle for fraud, embezzlement, money laundering, bribes, and well any and every crime under the sun, Bitcoin et el crucially acts as a pressure release valve to funnel dollars (FRNs actually) into in order to keep hyperinflation in check until...

The flood gates open and hyperinflation is deliberately allowed to explode (think holding a beach ball deeper and deeper under water over time and then suddenly letting it go) and the newly valueless dollar is then, right on cue, replaced with programmable slavery protocol CBDCs...

Which...

The public got conditioned into accepting because of the introduction of Bitcoin et el.

By the way, there are documents detailing digital currencies dating back to the 90s. The above was the plan all along:

BIS Chief Agustin Carstens: You Will Not Use Our CBDCs Without Our Permission (In Real Time): https://old.bitchute.com/video/mLVkHURKZp3S [1min]

"A key difference with the CBDC [and cash] is the central bank will have _absolute control_ on the rules and regulations that will determine the use of that expression of central bank liability--and we will have the technology to enforce that."

They're saying they will determine how you use > their < money, in real time. Obviously we cannot allow that. Here is a comprehensive breakdown of the hell this would create over time:

HELL ON EARTH IS COMING WITH CBDCs - Here is How: https://old.bitchute.com/video/C8Dm3BjdJm14 [15mins]

AI Overview

Stocks, bonds, and Treasuries are the primary investment vehicles in financial markets, differing fundamentally in ownership rights, risk, and return potential.

Stocks represent ownership in a company.

Bonds represent a loan made to a company or government.

Treasuries are a specific type of bond issued by the U.S. government.

1. Stocks (Equity)

When you buy a stock (or share), you are buying a small part of a company.

Returns: Profits come from capital appreciation (selling at a higher price) or dividends (profit sharing).

Risk: High. Stock prices can fluctuate significantly, and the company could fail, causing the stock to become worthless.

Goal: Long-term capital growth.

2. Bonds (Debt)

When you buy a bond, you are lending money to an entity (a company or government) for a set period.

Returns: The issuer pays you regular interest (often called a coupon) and returns the original loan amount (principal) upon maturity.

Risk: Moderate. Risks include interest rate changes, inflation, or the issuer defaulting.

Goal: Income generation and capital preservation.

3. Treasuries (Government Debt)

Treasuries are bonds issued by the U.S. Department of the Treasury to fund government operations.

Risk: Considered virtually risk-free because they are backed by the U.S. government.

Types:

T-Bills: Short-term (4 to 52 weeks), sold at a discount, no periodic interest.

T-Notes: Medium-term (2 to 10 years), pay interest every six months.

T-Bonds: Long-term (20 or 30 years), pay interest every six months.

Returns: Generally lower than corporate bonds due to the safety.